.png?table=block&id=1d2add1f-4b82-80b7-b5c6-cce6e9efcd20&cache=v2)

Post SEO title

The Trust Cost of Payment Processing

Meta description

Interchange+ pricing sounds transparent—but it hides most transaction fees. Discover what you’re really paying and how to avoid hidden payment costs.

Did you know that when you're quoted an "interchange +” pricing model, you're only seeing a small portion of the actual payment processing costs you'll incur?

The "plus" refers to the markup charged by payment processors like Stripe, Opayo, or Clover—but the majority of the costs come from other parties involved in the transaction. These significant fees are often overlooked in the quoted price.

The reason you’re only shown the processor's markup is that interchange fees—typically the largest part of the cost—are fixed and unavoidable for all businesses. Since you can’t influence these fees, they’re left out of the headline rate, even though they make up the bulk of what you’ll pay.

When quoted 0.3% for visa debit cards, by the time all the other fees are added on, you could be paying more than 1.1% in the UK. To learn more about the real-cost, see the data below (but all the prices from card schemes and interchange are deliberately complicated and opaque and unpicking them can take a full time person!).

Visa (EEA pricing here)

Interchange Plus pricing sounds transparent — and it can be — but it's only one piece (and often the smallest peice) of the puzzle. Interchange rates are just the fees set by card networks (like Visa or Mastercard), and the “plus” refers to the markup your processor charges. But here’s the catch: this doesn’t include all the other fees that happen in a transaction.

Here are just a few examples of what’s often not included in that headline rate:

- Assessment Fees (charged by the card brands)

- Gateway Fees

- PCI Compliance Fees

- Monthly or Annual Account Fees

- Batch Fees

- Chargeback Fees

- 3DS fees

- Cross-border or Currency Conversion Fees

So while the “interchange plus” rate might look competitive on paper, the total cost of processing could be much higher once all those other fees are factored in. That’s why it’s important to look at your entire statement, not just the advertised rate.

When you are offered “interchange +” pricing, you are only being quoted for the markup payment processors charge, which is the smallest part of the transaction

When you use your bank card, four parties are involved:

- You (the cardholder)

- Your bank (issuer)

- The business (merchant)

- The business's bank (acquirer)

How payments work:

- Both banks process the payment securely and promptly.

- When your bank sends funds to the merchant’s bank, it retains a small interchange fee.

Types of fees involved:

- Interchange fee (kept by your bank):

- Covers fraud prevention, system upkeep, and customer service.

- Enables banks to offer card services and invest in innovation.

- Largest portion of transaction costs.

- Merchant Service Charge (retained by acquirer):

- Includes interchange and fees for services like payment guarantees and terminals.

- Negotiated between merchant and their bank—Visa doesn’t set this.

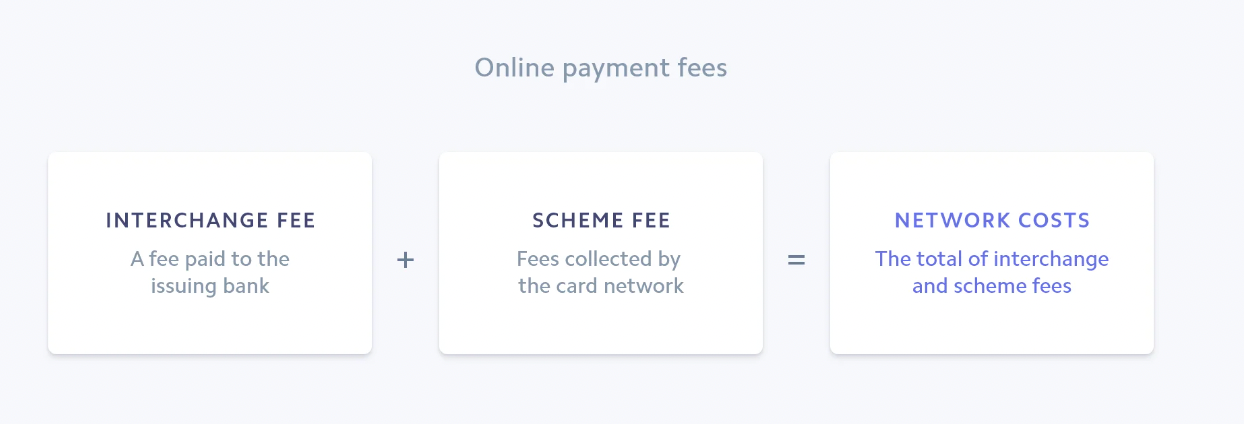

- Scheme fees (collected by networks like Visa/Mastercard):

- Cover services like authorisation, cross-border processing, and refunds.

Network costs depend on:

- Card type (e.g. rewards vs. non-rewards)

- Transaction location and channel (in-person or online)

- MCC – Merchant Category Code (learn more)

Additional notes:

- Interchange typically makes up the majority of network costs.

- Paid to the issuer for providing cards and onboarding customers.

- Scheme fees are collected by card networks and may include:

- Authorisation fees

- Cross-border fees

- Refund processing

- Other network services

- American Express operates on a different model as issuer, acquirer, and network. Its combined fee is called a discount rate.